By John W. Diamond, Ph.D., Director, Center for Public Finance, and

George Zodrow, Ph.D., Allyn R. and Gladys M. Cline Chair of Economics, Rice University

The Congressional Budget Office (CBO 2018) warns that under current law, Old-Age and Survivors Insurance (OASI) benefits must be reduced to the amount that could be financed with current payroll tax revenue once the OASI trust fund is exhausted. CBO (2018) projects that the OASI trust fund will be exhausted by 2032. The most recent Social Security Trustees Report (2019) projects that the trust fund will be exhausted in 2034 and that after that scheduled benefits would have to be reduced by 25 percent in the absence of any changes in fiscal policy. While these projections are dependent on several uncertain factors, it is clear that unless Congress acts, Social Security benefits will be reduced after the exhaustion of the trust fund.

In December 2018, the CBO hosted a symposium that focused on learning more about the effects of a reduction in OASI benefits, utilizing several models that could be used to examine such a policy analysis. The symposium included seven economic modeling groups that use computational overlapping generations (OLG) models. CBO asked each group to examine the effects of reducing current OASI benefits by one-third in 2031. A version of the results was presented at the National Tax Association’s 49th Annual Spring Symposium in Washington, DC on May 16, 2019. Diamond and Zodrow participated in the session along with six other prominent economic modeling groups. The other modeling groups included CBO, EY QUEST, Overlapping Generations USA, the Global Gaidar Model group, the Joint Committee on Taxation (JCT), and the Penn Wharton Budget Model group (more information about each model is available in the CBO presentation from the NTA Symposium).

The CBO asked each group to implement a set of assumptions about the reform in an effort to increase the comparability of the predicted reform-induced economic effects across the models. However, differences in modeling structure still remain and must be considered. This blog post presents results on the predicted changes in the major economic aggregates, including Gross Domestic Product (GDP), the capital stock, labor supply, and the ratio of public debt to GDP. These results are shown in Figures 1-4, which are taken from the CBO presentation discussed above.

Each modeling group reported results for a time path of each of the aggregate variables listed above in response to a specific reform. The reform was a reduction in OASI benefits equal to one-third of currently scheduled benefit payments beginning in 2031. The modelers assumed the reform was announced 13 years before 2031 and agents in the models anticipated the reform immediately. Over the period 2031-2051 the debt to GDP ratio was allowed to vary endogenously. After 2051, the debt to GDP ratio was held constant at the 2051 level by changing government consumption.

Model Projections

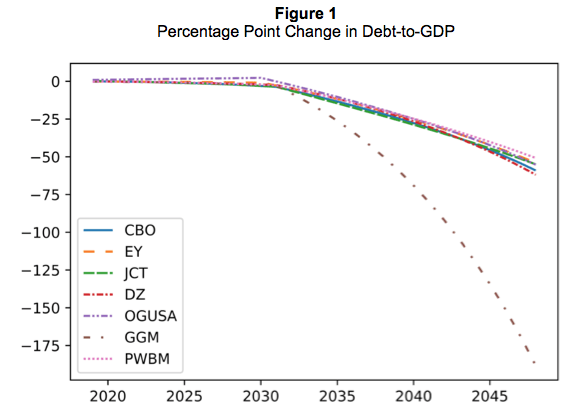

Figure 1 shows the simulated paths of the debt-to-GDP ratio from 2018-2048 for each of the models. Six of the seven models projected that the debt-to-GDP ratio would fall by about 50 percentage points by 2048. For example, the DZ model projected the debt-to-GDP ratio would fall by 62 percentage points by 2048.

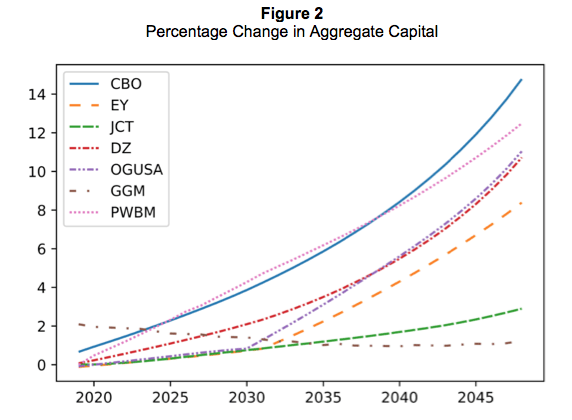

Figure 2 shows the simulated paths of the capital stock for each of the models. The variance in the simulated path of the capital stock is relatively large across the models, compared to the estimates of the debt-to-GDP ratio. The differences are driven by several factors including differences in the elasticity of saving across models, in each model’s assumptions regarding the movement of foreign capital across countries in response to the reform, and in how interest payments on the government debt are modeled. The reduction in OASI benefits would reduce consumption of goods and services and increase the amount of time spent working, thus increasing national saving. This would show up as an increase in public saving (e.g., a reduction in debt-financed consumption) and an increase in private saving as individuals save more to replace the reduction in retirement benefits. In a closed economy, the increase in savings would be the sole determinant of the change in investment and the capital stock. In an open economy, investment would be determined by new savings at home as well by savings from abroad that are invested in the United States. Diamond and Zodrow find that the capital stock is 10.7 percent larger by 2048 relative to baseline values.

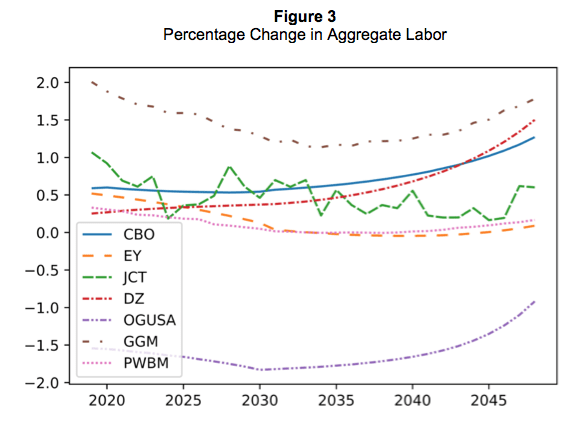

Figure 3 shows the simulated path for the level of employment in terms of hours worked for each model. Differences in labor supply are driven by two factors. The sensitivity of the supply of labor to changes in real and nominal wage changes is different across the models, and thus changes in OASI benefits will lead to different labor supply responses. In addition, increases in the capital stock will lead to an increase in the real wage and thus in the supply of labor. Diamond and Zodrow show that labor supply will increase by 0.2 percent initially and by 1.5 percent in the long run, relative to baseline values. This is similar to the increase in labor supply predicted by the CBO.

Figure 4 shows the simulated path of GDP relative to the baseline for each model. GPD is a function of the capital stock and labor supply. Both the capital stock and hours worked are larger than their baseline values, which implies that GDP must be higher than it was in the initial equilibrium. We find that GDP increases by 2.3 percent in 2048, relative to its baseline value.

Conclusion

This analysis highlights the dire need for fiscal policy reform and indicates clearly that implementing significant policy reforms is needed. The results from the various modelers show that a permanent 33 percent OASI benefit cut starting in 2031 reduces the debt significantly but does not solve the fiscal imbalances facing the United States. In addition, it is clear that while the various simulations mostly agree on the signs of the various economic effects of such a reform, the magnitudes of the effects are quite uncertain. It is widely known that acting sooner to bring our fiscal house in order is better than putting off the inevitable. The reform analyzed in this paper is not meant to be a policy proposal, but instead is an illustration of the magnitude of the problem and the difficulty of measuring the economic effects of such a policy reform. It is imperative that Congress starts to analyze serious solutions to the fiscal problems facing the United States.

References

Congressional Budget Office, 2018. The 2018 Long-Term Budget Outlook. Available at www.cbo.gov/publication/53139.

Social Security Administration, 2019. The 2019 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds. Available at http://www.ssa.gov/OACT/pubs.html.