By Mark Finley

Fellow in Energy and Global Oil, Center for Energy Studies

Since Russia invaded Ukraine, Saudi Arabia has made clear that it is not going to change oil policy. The Saudi leadership has repeatedly rebuffed requests from President Biden and leaders of oil-importing countries to accelerate production increases — a key factor behind the release of strategic oil stockpiles by the U.S. and its allies in the IEA. Recent monthly meetings of the OPEC+ group have taken less than 15 minutes to agree on a continuation of the plan put in place last year. A large diversion of Russian oil to India — and a corresponding reduction in Indian purchases of Saudi oil — hasn’t elicited public comment from Saudi oil officials even though Aramco tends to guard jealously its market share among large Asian growth markets.

Saudi relations with the U.S. are at a low point, and the OPEC+ partnership with Russia has paid big dividends for the Kingdom. With higher oil prices, Saudi GDP grew by an annualized rate of 9.6% in the first quarter — the fastest pace in over a decade. The Kingdom and its regional allies have abstained — or voted against — U.S. and European initiatives at the U.N. aimed at isolating Russia.

So, oil consumers under duress need to look elsewhere for relief.

But is that the whole story? Behind the scenes, the Saudis may be ‘playing ball’.

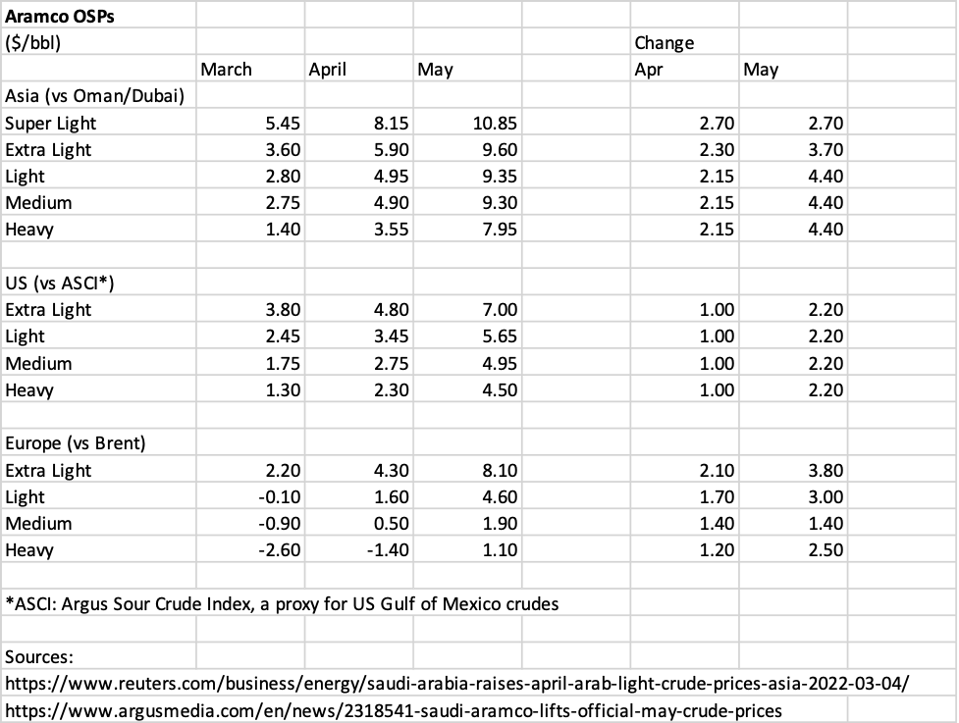

Each month the Kingdom sets prices for its crude oil exports. While state company Saudi Aramco does not publicize its pricing decisions, enterprising reporters are able to get the quotes from Saudi customers. These quotes are not for an actual price; rather, Aramco sets a “differential” for each grade of crude relative to regional benchmark crudes for Asia, Europe and the U.S. For example, a price for Arab Light delivered into Europe for March delivery was set at Brent minus 90 cents per barrel (see table below).

Table 1. Aramco OSPs

Sources: Compiled from Reuters and Argus Media

Saudi Aramco’s global marketing organization — with offices in key cities throughout the world — follows regional oil market developments very closely, and this allows them to fine-tune differentials based on subtle regional shifts in market fundamentals. For example, if Asia needs more diesel fuel, Aramco might price crudes that yield a higher share of diesel to be directed toward Asian markets. It is an incredibly efficient and well-informed organization, allowing the Aramco to maximize revenues from its oil sales within the policy framework set by the Energy Minister.

Aramco’s regional prices since the Russian invasion of Ukraine paint a very interesting picture of Saudi intentions over the past few months — a picture that may be at odds with the Kingdom’s public stance.

For deliveries in both March and April, Saudi prices for sales into Asia soared to record levels. Importantly, this is not a reflection of strong regional demand. Chinese demand has been impacted by renewed COVID-related shutdowns. And as noted earlier, India has dramatically ramped up purchases from Russia and reduced purchases of Saudi crude.

In these circumstances, a marketing policy of maintaining sales into a weakening regional Asian market should see the Kingdom cutting its regional differentials relative to Europe and the U.S. While Aramco’s European and American differentials have increased, they have not increased as rapidly as Asian differentials — especially for Arab “medium” — the Saudi crude that is the closest substitute for the main Russian export blend, Urals (see table above).

So why would the Asian differentials be raised so rapidly relative to Atlantic basin differentials? Recall that Aramco sets regional differentials to maximize revenue within the framework set by the Energy Minister. If Saudi decision-makers decide on a policy that moves crude from one market to another, Aramco prices its crude to accomplish that objective. For decades from the mid-1970s until the early 2000s, the Kingdom frequently discounted crude for sales to the United States with the objective of being the country’s top supplier.

In other words: Recent differentials could signal an intent to quietly steer crude into Europe to replace Russian supplies given growing refusal of European companies to purchase Russian oil — without publicly taking sides in a dispute that involves a critical OPEC+ partner. Other Middle-Eastern suppliers may also be playing ball: The UAE is similarly, and quietly, shipping more crude to Europe.

On one level, that’s how things should work. The oil market is massive, and traders are very creative. The global system is constantly adjusting regional prices and flows to accommodate ever-changing local supply-demand balances. It’s reassuring that things are working as they should. But the pricing decisions being made by Saudi Arabia also indicate this this isn’t just happening organically — rather, it is a deliberate choice being made by the Kingdom.

And admittedly, this is not a policy of adding extra barrels to the market. But it does appear to be a policy of helping European buyers adjust more smoothly in their efforts to reduce purchases of Russian oil. In that sense, it seems to be more of an effort to avoid further price volatility than about lowering prices.

Will the Kingdom continue with this approach? Will it tolerate losing market share to Russia in growth markets in Asia in contravention of its long-term strategic objectives? Are these pricing decisions a marketing maneuver or a deliberate policy choice? How would the Saudis react to a full EU embargo of Russian oil purchases? Only time will tell … especially since no formal announcement has been made by the Saudi government or Aramco. And since the price formulas are announced every month, we won’t need a lot of time to tell!

But for now, with the U.S. Congress and Administration considering punitive legislation aimed at the Kingdom and its allies for boosting world oil prices, this might be sign of quiet cooperation from the Saudis. A sign so quiet that’s easily missed.

This article originally appeared in the Forbes blog on May 4, 2022.