By Rachel A. Meidl, LP.D., CHMM

Fellow in energy and environment, Center for Energy Studies

Kenneth B. Medlock III, Ph.D.

James A. Baker, III, and Susan G. Baker Fellow in Energy and Resource Economics; senior director, Center for Energy Studies

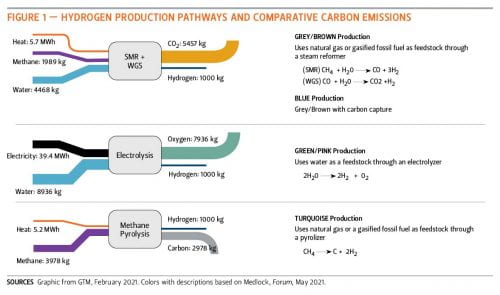

Decarbonization efforts and commitments from governments and industries are rising due to global climate and sustainability targets, and many are exploring and adapting innovative technologies and business models with the goal of zero-carbon or low-carbon energy and carbon utilization strategies. Hydrogen, a zero-carbon energy carrier that can be stored prior to use, has the potential to significantly transform the global energy landscape. It could be a cheaper energy option for freight transport and heavy trucks than electrification, and could be used in industrial process where electrification is difficult and costly. Multiple pathways for hydrogen production are available. Each is often differentiated by the color spectrum (Figure 1), but the majority of them have not been commercialized at scale.

For hydrogen to be low carbon, the negative CO2 externality must be abated, which pushes the production technology options away from grey and brown, which represent the dominant production technology deployed today, to other options. “Turquoise” hydrogen presents an interesting opportunity because it introduces a carbon-to-value proposition that can improve the commercial viability of the technology. In particular, the solid carbon that is recovered during hydrogen production via pyrolysis can be used in existing applications that involve carbon black, graphite, carbon fiber, carbon nanotubes (CNTs), graphene and other derivatives. Moreover, it can be applied in various applications, ranging from new advanced carbon materials to soil amendments, across different economic sectors, such as construction, transportation, and agriculture. The resultant impacts for CO2 emissions are potentially enormous because not only is energy use decarbonized, other CO2-intensive materials, such as metals and concrete, are displaced. Hence, by utilizing a methane pyrolysis process to create hydrogen and solid carbon, turquoise hydrogen taps into existing hydrocarbon value chains without CO2 emissions associated with the process.

Solid Carbon: Classification Matters

The management of solid carbon from pyrolysis is largely contingent on its regulatory classification. For example, classifying it in the “waste” category sets it on an alternate path for special handling, treatment, and disposal. Classification as a hazardous waste, nonhazardous waste, by-product, co-product, spent material, secondary material, or nonhazardous secondary material all determine regulatory obligations as well as operational, engineering, and administrative controls, which include accumulation time, storage limits, training and reporting requirements, etc. Moreover, classification will determine how solid carbon will be handled, where it can be stored, how it will be transported, and how and where it can be treated and disposed. None of this is settled.

Classification is complicated by the fact that not all methane pyrolysis processes yield an identical carbon output. The quality, morphology, and chemical constituents of the resultant carbon material can differ depending on the type of methane pyrolysis technology employed (thermal, catalytic, plasma) as well as the operating parameters used in process (temperatures, pressure, natural gas feed, methane conversion, reactor space, power, etc.). Although impurities can be processed and removed, the economics of stabilization and removal may be cost prohibitive.

Carbon black and carbon-based nanomaterials are a manufactured product with well-controlled properties, whereas black carbon is an incomplete combustion byproduct of fossil fuels. Comingling terms can lead to erroneous analysis of safety risks and prevent solid carbon from pyrolysis from being applied for “beneficial use” in remediation or soil amendment pathways. It could also drive consumer misperceptions that impede solid carbon from gaining traction as a value proposition that has the potential to displace or supplement energy intensive materials. Hence, to avoid unwarranted negative public perceptions, classification and clear definition is critical. Any negative public perception, whether or not it is rooted in science, can present a significant barrier to scale. Hence, it is important to maintain transparency in life-cycle data as well as public communication on any environmental and public health concerns of solid carbon materials.

Solid Carbon Uses: Scale is Critical

In order for turquoise hydrogen to be viable and competitive, the co-generation and sale of solid carbon as a feedstock into other processes is needed. The value proposition of methane pyrolysis relies on the availability of sufficiently large markets that can absorb the solid carbon output that will result from the scale-up of turquoise hydrogen production. However, the existing potential market outlets for solid carbon, primarily carbon black, is approximately 16.5 MMT. This is grossly insufficient. Current hydrogen production in the U.S. is 10 MMT, meaning the market for solid carbon would need to be at least 30 MMT annually if all existing hydrogen production were to switch to pyrolysis, and this doesn’t even account for growth. Thus, if turquoise hydrogen production via methane pyrolysis is to be scaled to meet a significant portion of energy demand, the applications for a burgeoning carbon supply chain would need to move beyond traditional markets. Either new market opportunities must open concomitantly with the scale-up of pyrolytic hydrogen, or storage options must avail themselves until a robust carbon market can develop.

Solid Carbon “Storage”

The storage of solid carbon could provide an interim solution that allows technologies to evolve and advanced carbon applications to mature. Existing research on the benefits of biochar, as one example, opens the possibility of the use of solid carbon as a soil amendment to reduce requirements for fertilizer and water in agriculture, and/or as a means to mitigate soil contamination by immobilizing heavy metals and organic pollutants. The latter option opens pathways for solid carbon to remediate EPA-designated Superfund sites, decommissioned military sites, former federal facilities, industrial sites with contaminated or disturbed soils, and other potential applications. Additional options for solid carbon are landfill applications or long-term storage in abandoned mines, access to which may already be available along existing rail infrastructure, thus removing a potential logistical challenge. Admittedly, such applications are not necessarily ideal or consistent with the principles of sustainability or a circular economy, but could nevertheless be explored as short-term solutions while commercially viable pathways for utilizing solid carbon develop.

As researchers and collaborators at Rice University’s Carbon Hub have found, it may be possible to manufacture advanced solid carbon morphologies with controlled properties. Over time, the conductivity of fibers made of CNTs, the ability of CNTs to convert heat into electricity, and the development of new advanced carbon materials could support a diverse range of products ranging from major electrical components (motors, power cables, umbilicals, undersea cables, etc.), to wearables, to energy storage devices, to aerospace applications, to transportation and more.

Looking Ahead

The challenges of developing a hydrogen and advanced solid carbon economy are vast. Identifying and appropriately addressing issues such as (1) negative public perception, (2) opposition to decarbonization strategies based on natural gas and hydrocarbons, (3) perceived risk of adequate long-term natural gas supplies, (4) the logistics of solid carbon transport, storage, and reuse, and (5) environmental, human health, and safety implications are all important considerations. Knowing the “what, where and how” regarding potential risks, barriers and strategies to navigate them to drive investment will help shape the future of innovative energy and materials production. It will also create viable pathways for solid carbon to provide a positive value proposition that supports broader scale hydrogen production, and facilitates achieving climate and sustainability goals.

This article originally appeared in the Forbes blog on September 22, 2021.