by Kenneth B. Medlock III

James A. Baker, III, and Susan G. Baker Fellow in Energy and Resource Economics

Senior Director, Center for Energy Studies

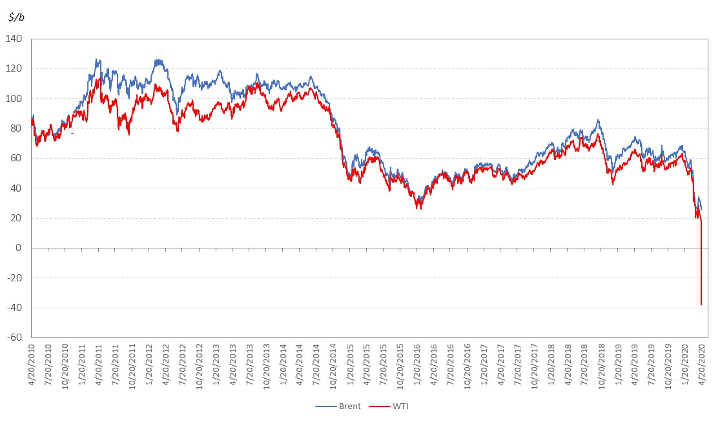

First, it must be understood that the prices quoted in the headline, and more generally on various media outlets, are futures prices for physical delivery of crude oil in the coming (or prompt) month. Typically, the prompt month futures price settles at a level that is consistent with the spot price indicator of physical market balance. This captures the notion of convergence that we are taught must occur to eliminate arbitrage opportunities. In other words, if the prompt contract futures price settles well below the spot price, it should indicate a profit opportunity where one buys the futures contract, takes delivery, then sells spot. Due to this dynamic, we often rely on the prompt contract price as a good indicator of current physical supply-demand balance, and hence spot price.

April 20 revealed something that many people found to be outright unbelievable; the price for May 2020 delivery of WTI crude (i.e. – the prompt contract price) collapsed by more than $50/b into previously unchartered, negative territory. Moreover, WTI disconnected from its typical relationship with Brent and petroleum product prices.

To begin, global crude prices tend to move together, allowing for differences related to transportation costs, physical constraints and crude qualities. For crudes of similar quality, such as Brent and WTI, the co-movement of price is even more pronounced, a reflection that crude oil is very fungible. So, any excessive differences are typically arbitraged away unless there are structural reasons preventing trade. Indeed, prior to the US lifting the long-standing ban on exports in late 2015, this was the case, as an inability to move light sweet crude was driving a disconnect between domestic pricing and international pricing. Moreover, the arbitrage moved downstream into refined products where there was no constraint on the ability to trade internationally. This was addressed in a previous Baker Institute study published in March 2015.

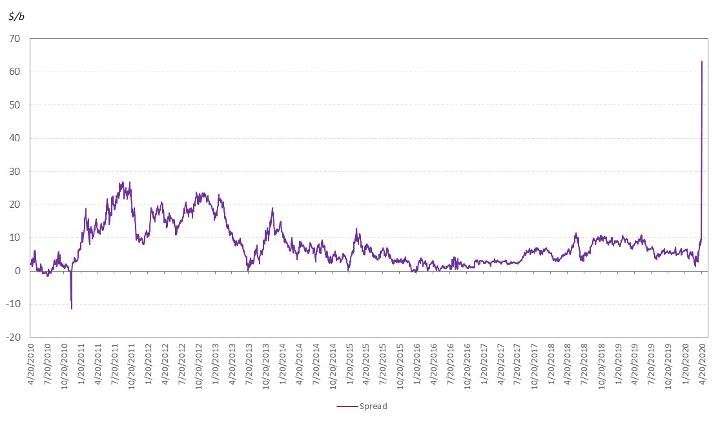

Historically, we do indeed see that prompt futures contract prices for Brent and WTI typically move together, as indicated in Figure 1, with the spread widening during periods when constraints on trade are realized, such as was the case between 2010 and 2015. In years leading up to 2010, the US was still a net importer of oil and petroleum products, meaning the point of arbitrage with the rest of the world was still onshore. Thus, WTI (as priced at Cushing, OK) tended to price slightly above Brent, even for the periods not pictured prior to 2010. But, with the dramatic growth in US oil production and the shift towards significant net exports of refined products, the point of arbitrage moved offshore, thus driving WTI into a discount to Brent. This did not indicate markets were not working; rather, it revealed that they were working quite well.

Crude oil and petroleum product prices also tend to move together (not pictured). This follows because supply-demand signals in the gasoline market, for example, directly impact the value of crude oil, and vice versa. This cointegrating relationship has a structural underpinning; after all, crude oil is a primary input into petroleum products. So, any large spread that emerges in the relationships between crude oil and petroleum product prices should present an immediate arbitrage opportunity that will be reflected in supply, demand and inventory movements of both crude oil and petroleum products.

Figure 1 – Prompt Contract Prices for WTI and Brent (Daily, 4/20/2010 – 4/20/2020)

Source: Data obtained from NASDAQ (www.nasdaq.com), author calculations

So what happened on April 20?

The prompt contract price for WTI disconnected from prompt contract prices for Brent and petroleum products. In fact, the discount of WTI to Brent at settlement for the prompt contract was in excess of $60/b. Moreover, the settlement price for the prompt contract for RBOB remained in line with Brent, not WTI. Why?

In short, storage capacity is overtaxed.

Of course, the discussion is deeper than this, or Brent and petroleum product prices would have dived as well, but they did not. We can start with the storage capacity situation at Cushing and a discussion of paper markets. In paper markets, such as crude oil futures, financial positions must be reconciled at contract expiry with physical delivery. Typically, a speculative financial position is opened with the intent to close (or offset) it prior to contract expiry. If an entity with such a position lacks the ability to take physical delivery (perhaps due to no access to storage or immediate demand), then that entity must liquidate its financial position in the futures market before the contract settles. All evidence indicates this is exactly what happened to the prompt contract for WTI. With no ability to store oil, large paper positions had to be liquidated. This indicates a massive oversupply of paper, not physical oil, thereby driving the contract settlement price down. In this case, it dove from $18/b to -$40/b before settling at -$37/b, all in less than a day!

Hence, the day’s activity was a signal of contract expiry approaching with no ability to unload long positions and no way for the holders of those positions to take physical delivery. Make no mistake, in normal circumstances neither of these things would have occurred. This is the result of a devastating collapse in demand that has occurred in the wake of the COVID19-driven economic shutdown, and is a realization of regional constraints (in this case storage becoming scarce) that can drive significant discrepancies across regional prices.

What comes next?

It is important to recognize that the global physical crude oil market is still pricing in positive territory. Yes, there are some regional spot prices that are in negative territory. But this indicates an extreme oversupply condition that is local, which should stimulate shut ins of immediately impacted physical production until demand can pick up to restore balance. The negative pricing signal we saw on April 20 for the May 2020 WTI contract settlement on the NYMEX is an indication of a financial long position that was too large to be physically accommodated. It also indicates an emergent (albeit temporary) reality that speculative long positions in crude oil futures will be punished as places to put crude disappear.

Whether or not this happens to the June contract will depend the evolving supply-demand balance, which will reflect production shut ins (which appear to be accelerating), near term demand recovery (which is still very uncertain and dependent on economic activity being restored), and the extent to which storage fills (which is itself a reflection of production and demand). So, given the uncertainties involved in the current oil market, April 20 could be a harbinger of things to come; or, it might not. Given the extreme volatility and associated downside risk, it is likely that production shut ins will accelerate over the next few weeks, which will alleviate mounting pressures on storage.

A natural question to ask is, “Is crude oil truly a valueless commodity at the margin now?” That’s precisely what a negative price indicates. But it is important to dig a little deeper before making such a proclamation. Indeed, we see positive values out along the forward curve for WTI, indicating the market still views crude oil to have some future value (See Figure 2). At the very least, an ability to buy May and sell June would yield a return that any trader would love to reap, but if arbitrage is capped by a lack of ability to store oil, then that opportunity is not on the table. Suffice it to say that everyone is scrambling for answers to the storage shortfall, as well as grappling with how long the current oversupply situation will persist. While the immediate term is rife with uncertainty, one thing is certain: oil market recovery cannot commence until the economy picks up.

Figure 2 – WTI Futures as of April 20 (May 2020 – May 2022)

Source: Data obtained from the CME Group website

The stories that will be told …

Looking longer term, the current market stress may bring the notion of position limits back into the limelight. Specifically, an argument that financial positions be “underwritten” by some minimum demonstrated ability to physically take delivery of crude oil may be a path forward. Such a rule could require, for instance, storage capacity (or at least a position in storage) for entry into the crude oil futures market. This begs the questions, “Would minimum physical delivery requirements encourage the development of commercial storage at the margin? And, if so, how much would that have helped in the current circumstance?” It is likely that non-physical interest in crude oil futures would wane, which would be the typical response if taking such positions is more costly. The cost of entry would be a fixed cost related to storage positions that may be a barrier to entry for some financial interests, which raises questions about market participation and competition. But storage capacity would also expand, and its utilization would be in the hands of commercial interests. This, in turn, increases physical fungibility, which serves to reduce volatility. The cost-benefit of such an outcome is an interesting area of exploration.

Only time will tell what future regulatory guidance may bring, but the die has been cast for the status quo to, at the very least, be challenged.

This post originally appeared on the Forbes blog on April 21, 2020.